Consultancy Quinlan & Associates says Hong Kong’s eight virtual banks are poised for massive growth in revenues and a slice of deposits. It estimates by 2025, the neobanks could grab up to HK$76 billion ($9.7 billion) of per annum revenues, and a combined revenue market share of 19.3 percent.

Those numbers are based on the firm’s estimate of the current banking market size of HK$373.0 billion ($47.9 billion) in annual retail, commercial, and corporate banking revenues. Currently, the big four incumbents – HSBC, Standard Chartered, Bank of China, and Hang Seng Bank – dominate 62 percent of deposits and 54 percent of loans, the consultants calculate.

In light of the rapid speed with which neobanks (another term for branchless banks) have gained customers in markets such as the U.K., the Hong Kong industry could obtain a large user base. But a fifth of the revenue market is a large number: in the U.K., for example, neobanks still struggle with basics such as growing deposits.

Quinlan’s report acknowledges challenges to virtual banks’ growth. In a low-interest rate environment and the need to quickly scale their customer bases, virtual banks are more likely to chase fee-based income rather than adopt traditional deposits-based lending models.

Says the report: “We see ample scope for Hong Kong’s virtual banks to pursue a fee-based income model in coming years, offering products and services such as insurance plans, wealth management advisory, buy-now-pay-later credit lending, budgeting tools, investment products and trading services, and international multi-currency transfer and payment capabilities.”

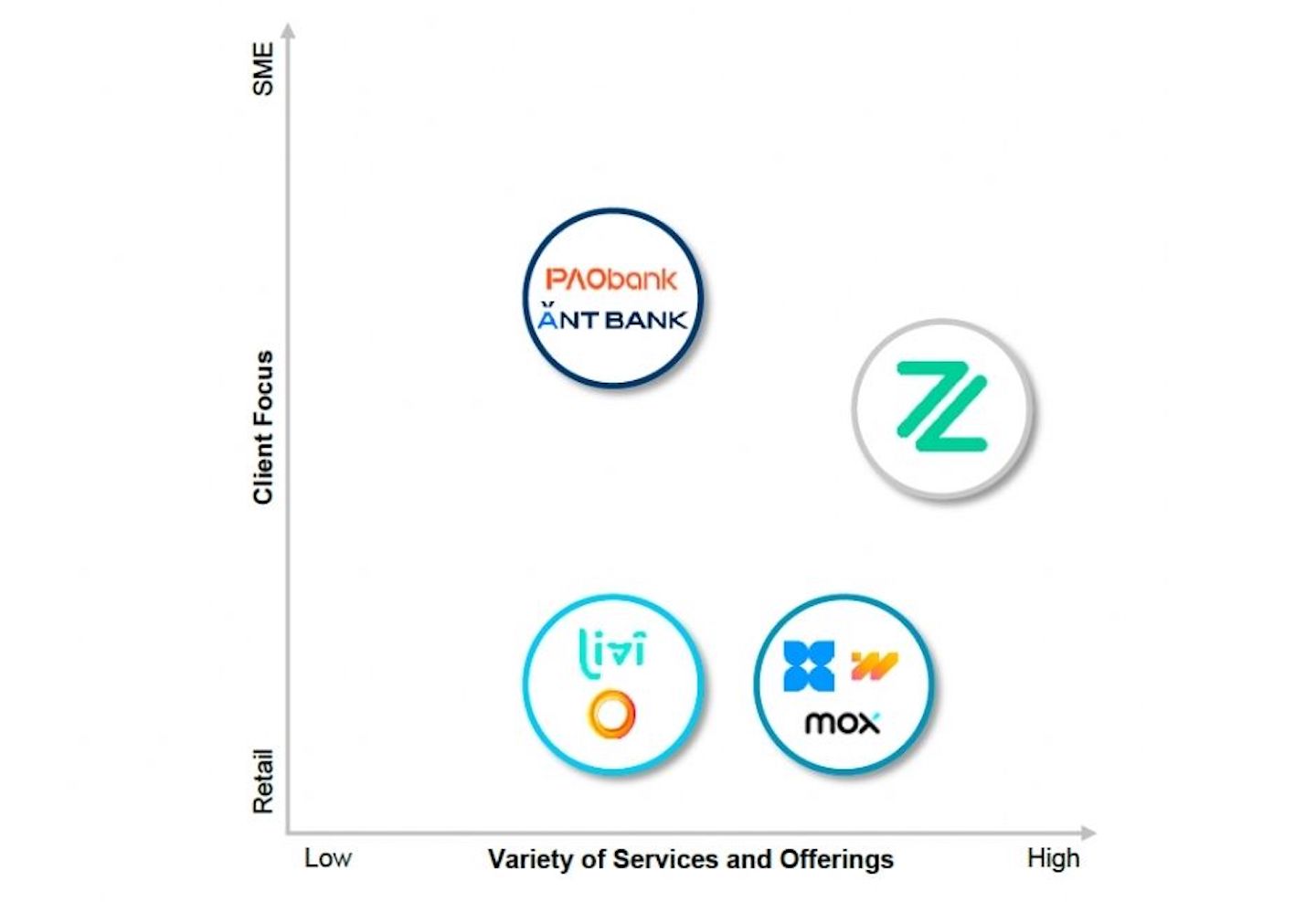

Market sizing

The firm’s market-sizing estimates suggest virtual banks will win up to 1.9 million customers by 2025. Its bullish figures on winning deposits extrapolates from Mox Bank’s claiming an average customer balance of over HK$70,000 and a total deposit base of HK$5.1 billion as of December 2020. Such a trajectory would take Mox to average retail customer deposit balances that are about half of HSBC’s and a total retail deposit base of HK$443 billion.

From there the firm projects virtual banks’ other businesses in wealth management, SME banking and corporate banking based on HSBC’s composition.

Quinlan & Associates reckons personal loans and SME loans will be the biggest credit product, and that they will lend at the relatively high interest rate of 9 percent on average. This leads to calculations about neobanks garnering HK$34 billion in interest income.

But the bigger gains should come from non-interest income, which the firm adds up to HK$42 billion, based partly on U.K. neobank performance.

To reach these targets, the eight virtual banks will have to grow market share per annum by almost 2.4 percent each, on average; and achieve annualized revenues of HK$9.5 billion.

To get there will probably involve consolidation. It is possible that new areas of growth will emerge if these banks can expand to serve customers in mainland China (under the Greater Bay Area rubric) or elsewhere.

The survey’s interviews with the CEOs of the eight virtual banks suggests their focus will be on rapid customer acquisition and differentiating product development. They also intend to leverage customer data in new ways in order to win commanding positions in niche market segments.

“We see a clear opportunity for the virtual banks to drive greater user activity and engagement, gradually winning over customer trust and, ultimately, wallet share,” the report says.