Perspectives

Unicorns, ten years on, face retrenchment – and rebirth

VC Aileen Lee, who invented the term ‘unicorn’, reviews a decade of growth and predicts a new boom.

It’s now been ten years since the term ‘unicorn’ was coined to mean a startup with a $1 billion valuation. The woman behind the term, Aileen Lee of Cowboy Ventures, has now released a report that updates the unicorn story.

Back in 2013, there were only 29 unicorns. Hitting a billion-dollar valuation was so rare that these companies were as common as, well, a unicorn. Most of them ten years ago were in consumer tech, and there was only one private company valued above $100 billion, which was Facebook.

Today there are 532 unicorns in the US, a 14-times expansion (Lee’s study only covers the US). Most of them are enterprise-focused, with OpenAI the new juggernaut in a class of its own (see figure below. from Cowboy Ventures).

Unicorns that are natives in AI and machine learning apps and infrastructure have emerged from nowhere six years ago to become 7 percent of all unicorns in the US, a trend turbocharged by the advent of generative AI-native companies.

Some of this expansion might be because of great founders or great tech, but in recent years it was a function of zero interest rates, which helped send 3 times more capital to startups than in the previous decade. That also meant three times more money going to VC fees.

- Read more:

- Will there be a gen-AI insurtech unicorn?

- Fintech VC | Herston Powers, 1982 Ventures | DigFin VOX Ep. 67

- Geopolitics scramble venture capitals’ global ambitions

Since the peak in 2021, the unicorn story has been a story of retrenchment. First, less money. Beyond the biggest VCs, many funds froze raising new money from institutional investors, and 40 percent of VCs stopped investing in new startups.

Second, a lot of unicorns turned out to be only valuable on paper. About four in ten of these tech companies now trade below $1 billion in secondary markets, so gradually as they seek new funding rounds even more of them are going to be marked down.

Cowboy Ventures says this cycle has a ways to go, and Lee expects the number of true unicorns will fall from 532 to 350 companies. The good news is these survivors will be healthy. That figure is still a 10x increase over the decade, and although Lee expects the next few years to be tough, she believes this retrenchment is setting the scene for another explosion in VC-backed tech companies, led by AI.

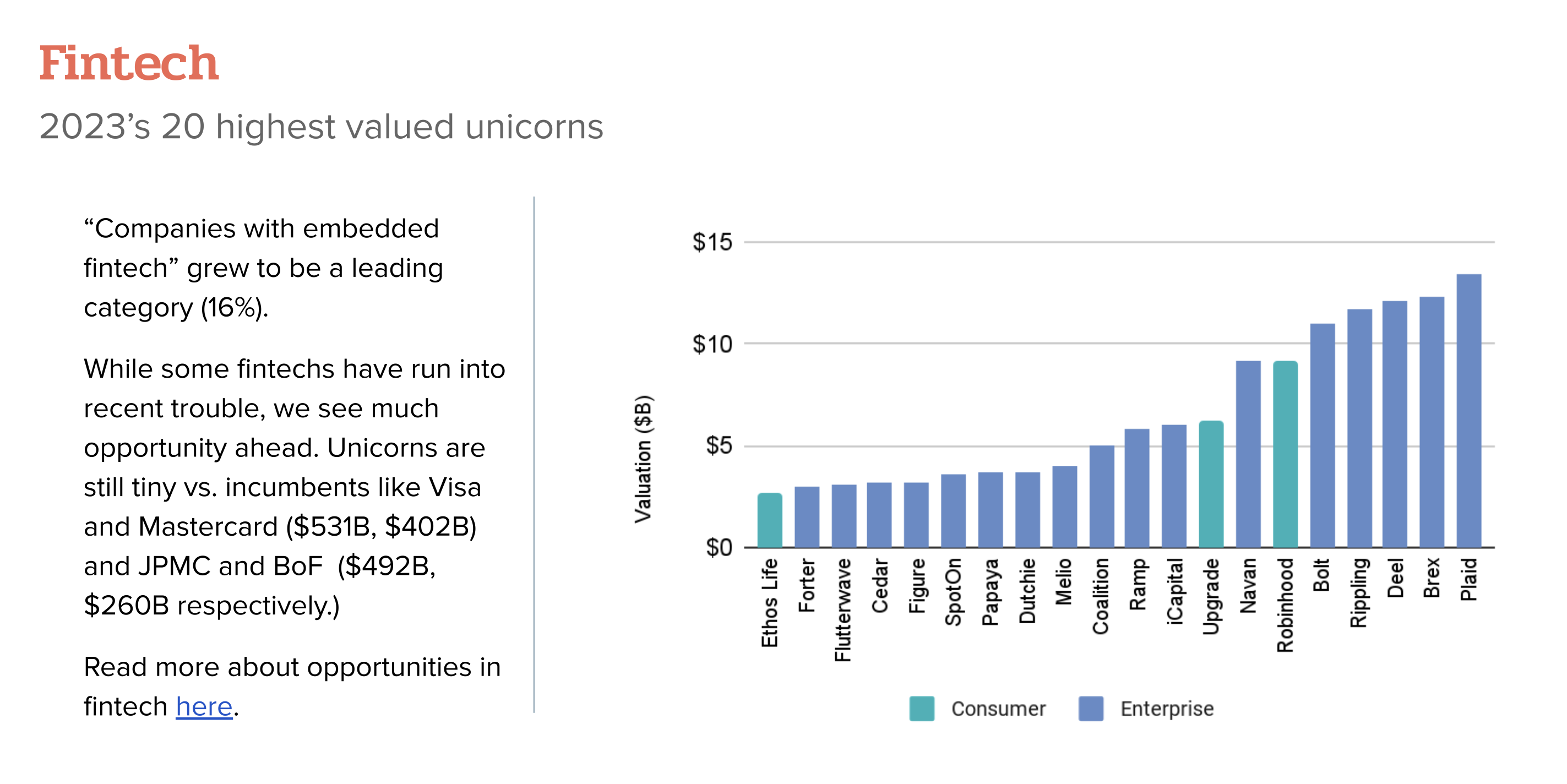

Lee and her co-writer, Allegra Simon, remain bullish on fintech, which over the past three years emerged as the mostly highly valued segment in the startup world. Either pure fintechs or companies embedding fintech now account for 16 percent of the universe in the US (see main image), led by Plaid (embedded banking) and Brex (credit cards and cash management for tech companies).

The report expects fintechs will continue to grow, noting they remain tiny versus incumbents in payments and banking, such as Visa, Mastercard, JP Morgan and Bank of America.

Cowboy is a little more cautious on the Wild West of crypto and Web3 startups, which enjoyed the highest valuations from the bubble, and saw the biggest drops in valuation and transaction volume. The report notes since 2022, 70 percent of crypto unicorns have not raised new funding, suggesting there will be more down rounds in this category.

The bad news is that over the past 10 years, despite the bubble, investors in VC funds didn’t do that great. Investors would have done better investing in public listed companies that began as unicorns, such as Microsoft, Salesforce and Amazon. The inflated valuations of the bubble years hid sloppy, FOMO-driven investing by VCs.

But software continues to reshape the world, and periods like today are where the next cohort of unicorns is being built.

Cowboy predicts the next 10 years will see the US unicorn community grow to 1,400 companies. “Previous downturns have been fertile for unicorn founding,” the report said. “This will be exciting for the future of innovation, jobs and the tech economy, despite current conditions.”

That’s true in many parts of the world, not just the US. VC-backed startups continue to transform the economies of India and Southeast Asia. Japan, traditionally not a VC-friendly place, is now embracing innovative startups.

VC’s greatest success beyond Silicon Valley has been China, which is now the only other country that boasts an equally broad and deep ecosystem, with VCs from angels to growth equity, industry specialists, an impressive domestic LP base, and a massive entrepreneurial pool. However, the government’s shifting priorities have made life difficult for VCs and entrepreneurs. The talent and the know-how is there, however, ready to move aggressively once conditions are more favorable.

Why the RWA revolution will not be televised

Dušan Stojanović: AI in fintech is a compliance story

Has ASX learned the lessons of its DLT failure? UPDATED

InDrive Money and Fingular enter Indonesia ride hailing